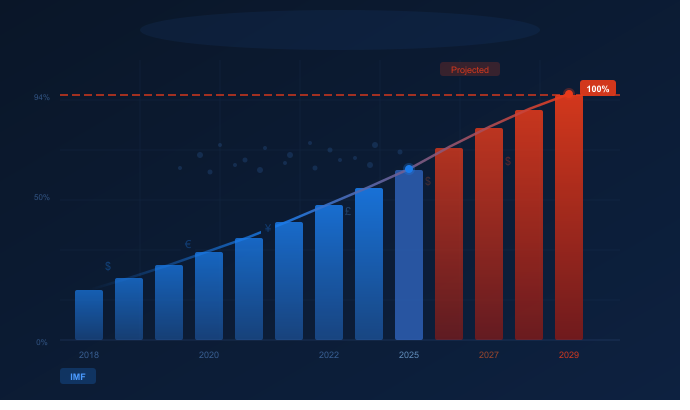

The International Monetary Fund has issued its most urgent warning about global debt in the organisation’s eight-decade history — and for the first time, the mathematics of the crisis have a specific and deeply alarming destination: 100 percent of global GDP, arriving one full year earlier than previously projected.

The April 2026 Fiscal Monitor, published under the title “Fiscal Policy Under Pressure: High Debt, Rising Risks,” represents the IMF’s comprehensive annual assessment of the world’s public finances. Its findings are stark. Global public debt rose to just under 94 percent of world GDP in 2025. By 2029 — one year earlier than the Fund’s previous estimate — it is projected to cross the 100 percent threshold. By 2031, global debt is projected to rise by an additional eight percentage points from current levels.

These are not projections from a pessimistic scenario. They are the IMF’s central, baseline forecast — before accounting for the downside risks that the Fund itself describes as dominating the outlook.

The Numbers Behind the Crisis

To understand what 100 percent debt-to-GDP actually means, consider the scale of the figure involved. In 2024, world public debt reached a record $102 trillion. That is $102,000,000,000,000 — more than the combined annual economic output of every country on earth.

This accumulation has been driven primarily by the world’s major economies — the United States, China, Japan and the large European nations — whose fiscal trajectories set the direction for the global financial system. The United States alone carries debt at approximately 122 percent of its annual GDP. Japan’s debt-to-GDP ratio exceeds 250 percent. These figures are not new, but the speed at which they are rising — and the deteriorating conditions in which they must be serviced — is unprecedented in the post-war era.

Over the past fifteen years, developing-country debt has grown at twice the rate of debt in advanced economies — a pace that reflects the combination of pandemic-era spending, commodity price shocks, climate-related disasters and the structural challenges of building social safety nets and infrastructure without access to cheap capital markets.

The Middle East War Factor

The IMF’s April 2026 World Economic Outlook, published alongside the Fiscal Monitor, added a new and serious variable to the global debt equation: the Middle East conflict. The outbreak of war has disrupted commodity markets, pushed global bond yields higher and introduced a level of financial market volatility that the Fund describes as significantly increasing since late February 2026.

Under the assumption that the conflict remains limited in duration and scope — which the Fund explicitly acknowledges may not hold — global growth is projected to slow to 3.1 percent in 2026 and 3.2 percent in 2027. Both figures are below recent outcomes and substantially below pre-pandemic averages. Global inflation is expected to tick upward in 2026 before resuming its decline in 2027.

The fiscal consequences of the Middle East conflict add directly to the global debt problem. Higher commodity prices translate into higher import bills for commodity-importing nations, larger fiscal deficits and increased borrowing requirements. Higher bond yields — driven by conflict-related uncertainty and inflation expectations — raise the cost of servicing existing debt while simultaneously making new debt more expensive to issue.

Three Economies That Could Default

The IMF’s Global Financial Stability Report, published in April 2026, identified a specific and alarming dynamic in the emerging market debt landscape that points toward potential sovereign defaults within the next eighteen months.

The Fund’s analysis identifies a structural vulnerability in how emerging market debt is now held. Approximately 80 percent of emerging market debt is now owned not by patient bank lenders who historically provided stability through market cycles but by portfolio investors — hedge funds, asset managers and pension vehicles — whose risk tolerance has grown significantly lower over time. This investor base is extraordinarily sensitive to shifts in global risk sentiment.

When conflict escalates, when inflation surprises on the upside, when the dollar strengthens or when financial conditions tighten — these investors sell emerging market assets rapidly and simultaneously, creating the kind of sharp capital outflows and currency pressures that can push already-indebted governments toward a debt servicing crisis.

The IMF did not name specific countries in its public warnings — doing so would risk triggering the very market panic it was describing. But the parameters the Fund outlined point toward economies that combine high external debt denominated in foreign currencies, low international reserves, heavy dependence on commodity exports and limited institutional credibility with financial markets.

The erosion of the US Treasury’s traditional status as the world’s ultimate safe-haven asset — what the IMF describes as the erosion of the Treasury’s safety premium — adds a further layer of complexity. For decades, investors fleeing risk in any corner of the world bought US government bonds, stabilising the global financial system even in severe stress periods. The April 2026 Global Financial Stability Report flags this premium as eroding — a shift with profound consequences for the global financial architecture that has operated since Bretton Woods.

The Spending Pressures That Will Not Stop

What makes the current global debt situation particularly difficult to resolve is that the pressures driving spending higher show no sign of abating — and most of them are not discretionary.

Social spending pressures are structural. Ageing populations across the advanced economies — Europe, Japan, South Korea, and increasingly the United States — are driving pension and healthcare costs inexorably upward. These are not political choices that governments can easily reverse. They are demographic realities that will compound for decades.

Defence spending is surging. Russia’s war in Ukraine, the Middle East conflict and the intensification of great-power competition between the United States and China have broken the post-Cold War assumption that advanced democracies could maintain strategic security with lean defence budgets. NATO members are racing to reach or exceed the two percent of GDP defence spending target. Many have already committed to higher levels.

Strategic autonomy spending — the industrial policy costs of reducing dependence on adversarial supply chains for semiconductors, critical minerals, pharmaceuticals and clean energy technology — represents a new category of fiscal pressure that barely existed five years ago. The United States, the European Union, Japan and South Korea are all running large-scale industrial subsidy programmes that add directly to public deficits.

Interest payments themselves are now a major driver of deficit expansion. After a decade of near-zero interest rates during which governments borrowed at minimal cost, the transition to a higher-rate environment has dramatically increased debt servicing costs. Governments that issued long-term bonds at low rates during the pandemic are now rolling over that debt at rates two, three or four times higher — locking in structural increases in their interest bills for years ahead.

What the IMF Is Asking Governments to Do

The IMF’s prescription — credible, well-sequenced fiscal adjustment across all country groups — sounds straightforward. In practice it is politically and socially enormously difficult.

The Fund calls for gradual reduction of primary deficits, structural economic reforms to boost productivity and growth, and stronger international cooperation to address debt distress in the most vulnerable economies. These recommendations are sensible. They are also the same recommendations the IMF has been making, in various forms, for most of the last decade — a period during which global debt has risen by tens of trillions of dollars.

The fundamental problem is that fiscal adjustment — spending cuts and tax increases — is contractionary in the short term and deeply unpopular with electorates that are simultaneously dealing with elevated inflation, housing affordability crises and stagnant real wages. Governments that attempt genuine fiscal consolidation frequently lose elections to parties that promise to reverse it.

What Ordinary People Will Feel

The consequences of the global debt crisis will not be felt only in financial markets and government treasuries. They will be felt in households and communities around the world through mechanisms that are already visible in many countries.

Public services will face sustained pressure as governments prioritise debt servicing over spending. Education systems, healthcare, infrastructure maintenance and social safety nets — the institutions that determine quality of life for most people — will be squeezed in countries that cannot borrow freely and cannot raise taxes quickly enough to meet both servicing costs and service demands.

Currency instability will affect the purchasing power of ordinary people in countries where the exchange rate deteriorates under debt pressure. Import costs rise, inflation accelerates and real wages fall — a combination that has historically been associated with significant social and political instability.

The countries most exposed to these consequences are not the major advanced economies — the United States, Germany, Japan and France can absorb significant fiscal pressure before reaching crisis conditions. They are the middle-income and lower-income emerging markets that depend on continued access to international capital markets at manageable rates. For those countries the margin between fiscal stress and genuine crisis is narrower than it has been at any point since the 1980s debt crisis.

The Road to 2029

The IMF’s projection that global debt will reach 100 percent of GDP by 2029 is not an endpoint — it is a milestone in a trajectory that, absent fundamental changes in fiscal policy, continues upward after that.

The Fund’s own modelling suggests that under current policy trajectories, the expected improvement in the global primary balance through 2031 will be insufficient to stabilise the global debt ratio — let alone reduce it. The world is, on current trends, adding to its debt burden in absolute terms every year through the end of the decade.

That trajectory is not inevitable. History provides examples of countries that have achieved substantial fiscal consolidation — Italy in the 1990s, Canada in the same decade, several emerging markets following IMF-supported adjustment programmes. But those adjustments required political will, institutional credibility and often significant short-term economic pain.

In a global environment defined by great-power competition, Middle East conflict, technological disruption and democratic political pressures, assembling those conditions simultaneously across the world’s major economies represents perhaps the defining governance challenge of the decade ahead.

GlobeBuzz will continue tracking global economic developments and IMF assessments as they evolve.

Follow @globebuzz_org on X and Telegram for live updates.